Responsible Lending

- Sustainable Finance Statement

- Decarbonization Policy

- Responsible Investment

- Responsible Lending

- Responsible Marketing

SinoPac Holdings understands the financial industry plays an important role in reducing global carbon emission, as it controls the majority of the cash flows supporting the economy. SinoPac Holdings incorporates ESG factors into its risk assessment process and pays close attention to clients' understanding towards the risks and opportunities brought by climate change as well as its impact on financial performance, in order to take proactive countermeasures further.

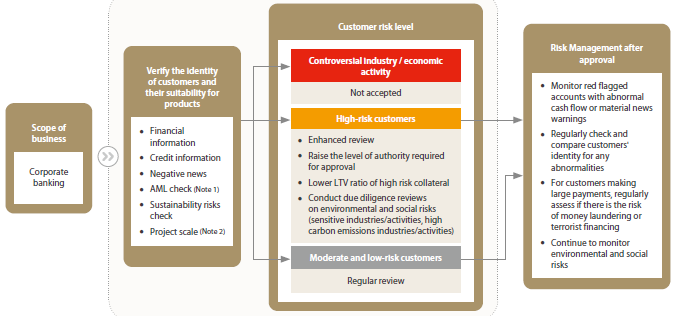

Corporate Banking Lending

KYC and CDD Processes for Corporate Lending

SinoPac Holdings incorporates ESG factors into its Know Your Customer (KYC) and Customer Due Diligence (CDD) procedures for lending business and implements classified management of corporate banking customers, carrying out reviews and management operations by risk level. Furthermore, the Company has enhanced ESG risk reviews for large project financing and continues to monitor environmental and social risks after approval.

- Note 1:Please see SinoPac Holdings 2022 Sustainability Report section 2.2.3.4 Customer Due Diligence.

- Note 2:If the project financing amount reaches US$10 million or above, its risk level must be determined according to the EPs.

Bank SinoPac's "Corporate Credit Risk Management Division" is the dedicated unit responsible for establishing guidelines relating to responsible lending and the EPs, and for planning a conducting ESG credit risk analysis. The Division continues to monitor trends in ESG risks of each industry and their impact on the Bank's operations. In terms of execution, front line corporate banking personnel are responsible for disclosing and specifying the ESG risks of clients. Corporate banking credit review personnel are then responsible for checking and reviewing the analysis of ESG factors in credit applications. Corporate banking and credit review personnel jointly complete due diligence of ESG risks.

Bank SinoPac established the “Responsible Lending Management Guidelines” and incorporate ESG considerations in the lending process. If ESG risk factor exists, the business unit shall engage with customers to explore the situation and assist customers to improve and respond by evaluating and proposing mitigative and remedial measures. In the event that customers involving in serious issues or cannot resolve issues continuing for a long time, the Bank should evaluate the business relationship in a prudent manner.

Review process and engagement includes:

- Prohibit controversial industries: e.g. pornography, controversial arms.

- Carefully Evaluate in Sensitive Industries: enhanced ESG risk analysis for sensitive industries, including oil and gas, coal-fired power generation, gambling, those with issues in food safety, toxic radioactive substance, non-medical and hazardous genetic engineering, non-adhesive asbestos fiber and polychlorinated biphenyls (PCBs) manufacturing.

- Follow the business restrictions imposed by the “Decarbonization Policy”of SinoPac Holdings.

- Incorporate ESG related factors, such as environmental, social, governance, and climate change risks etc., into the lending processes:

- Focus on industries/enterprises/economic activities with high carbon emission to strengthen climate resilience and support international trends for building a low-carbon economy. Bank SinoPac advises clients to provide data on GHG emission intensity and low carbon transition strategies, and engages in green lending to integrate industrial operations with the circular economy. If the client fails to provide the aforementioned transition plan after repeated rounds of communication, we carefully evaluate whether to continue to provide funding.

- Encourage clients to engage in socially responsible lending for reducing inequality, providing basic life necessities, or providing suitable work to create positive relationships, and avoid and resolve negative impact on stakeholders. The Company encourage them to make positive contributions to social goals without harming the environment.

- Focus on whether clients assess and respond appropriately to the risks and opportunities of climate change and natural capital, whether they understand the impact of climate change and loss of biodiversity (including conservation of species, habitat preservation, and environmental sustainability) on their financial performance, and whether they have taken response measures.

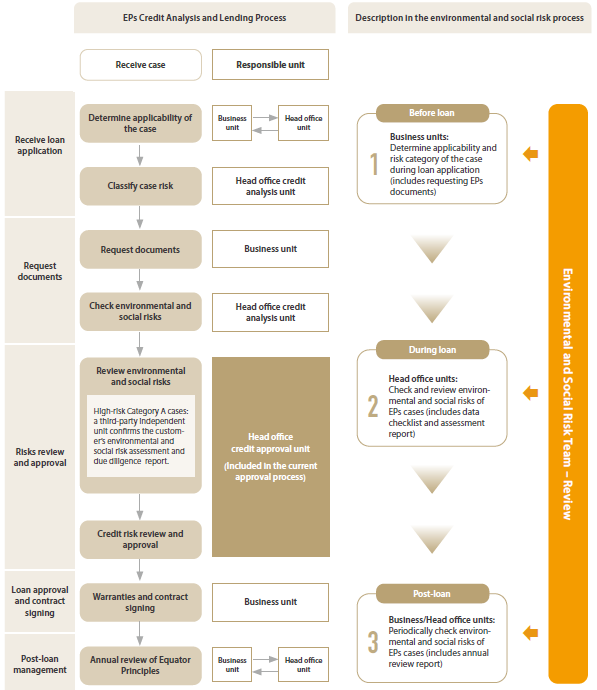

Equator Principles

Bank SinoPac formally became a signatory to the Equator Principles (EPs) in February 2020. Bank SinoPac established EPs related guidelines and operating procedures, completed EPs training sessions, and smoothly transitioned to EP4, strengthening the management of human rights risks and climate change risks in the credit analysis and lending process for project financing. Bank SinoPac established a dedicated Environmental and Social Risk Team in November 2021, serving as an internal consultant for the risk assessment and review of EPs cases. For high-risk cases, the team seeks assistance from a third-party external consultant according to the EPs. The Company has also incorporated Equator Principles cases into the self-inspection items starting from December 2022 and a third party from head office will inspect the process of Equator Principles cases regularly.

EPs Credit Investigation and Lending Process

Starting in 2022, Bank SinoPac discloses the industry, risk category, and designated or non-designated country of project financing, number of cases involving environmental and social risks management, and whether or not an environmental and social risks assessment report prepared by independent third-party experts is provided on the official website of the Equator Principles Association.

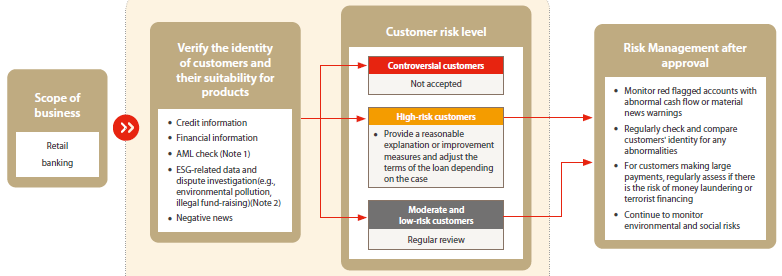

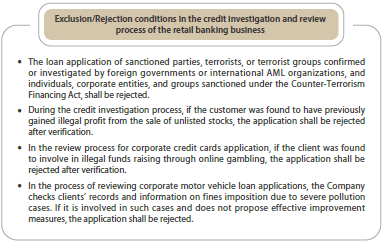

Retail Banking Lending

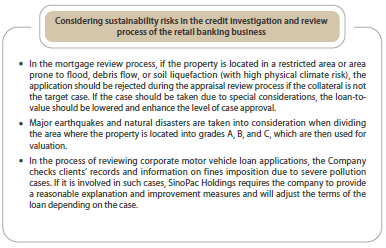

SinoPac Holdings incorporated ESG factors in its retail banking businesses (including mortgage, motor vehicle loan, credit loan, and credit cards). When a new retail banking loan application is received, besides carrying out KYC and CDD mechanisms, the Company actively investigates the customers’ ESG related information and uses the ESG risk they may face for risk grading, appraisal, and adjustment of loan terms.

KYC and CDD Processes for Retail Banking Lending

- Note 1:Please see SinoPac Holdings 2022 Sustainability Report section 2.2.3.4 Customer Due Diligence.

- Note 2:The environmental and social factors incorporated into related ESG surveys include whether the collateral is located in areas with regulatory restrictions and flood-prone areas and whether customers are implicated in penalties for polluting the environment, money laundering and terrorist financing, and illegal fundraising.

Customer Due Diligence is first conducted to verify the customer's identity and suitability for products. Transactions may be temporarily suspended if the customer does not cooperate with regular reviews, refuses to provide information on the beneficial owner or individual who exercises right of control over the customer, the nature and purpose of transactions, or the source of funds.

Furthermore, Bank SinoPac also creates a risk classification process in credit reviews, and divides customers into high, medium, and low risks of money laundering with a Risk Based Approach (RBA) based on their background, region, business dealings, transaction behavior, and services. The process is incorporated in the credit review system and different management measures are taken accordingly.

After approval, Bank SinoPac will examine if current retail banking credit products (car loan, credit loan, credit card) have major warning signs or potential abnormalities based on customer or case indicators (including product application approval rate, average annual interest, age of accounts, etc.), and will regularly track customers' credit status and payments. This will significantly reduce overdue loans and overdue receivables in our product portfolio, taking action to prevent potential ESG risks of bank services and funds.

If customers have any overdue payments, Bank SinoPac adopts different collection strategies based on the time payments are overdue. According to the debt negotiation mechanism set forth in the “The Statute for Consumer Debt Clearance” promulgated by the government, debtors who are unable to repay their loan for consumption, credit card or cash debt may submit an application to the bank for negotiation, and jointly formulate a feasible repayment plan with the bank. This approach helps people who have financial difficulties due to debt to have an opportunity to rebuild their life and economic status. For loans that cannot be collected, bad loans are regularly written off to maintain asset quality. When collection is outsourced, if the collection agency engages in improper conduct that is against the law or severely damages the Company's reputation, SinoPac Holdings will initiate emergency response procedures.